Tap your phone. Confirm. Done. Mobile payments have become one of the fastest, most convenient ways to pay — and in Europe, their adoption is accelerating. From supermarkets and train stations to e-commerce platforms and subscription services, mobile wallets and contactless technology are redefining the checkout experience. Paying with your phone is becoming a natural part of everyday transactions across Europe. In this article, we explore how mobile payments work, what makes them secure, and why merchants across the continent should treat them as a core part of their payment strategy.

What is mobile payment and how does it work in practice?

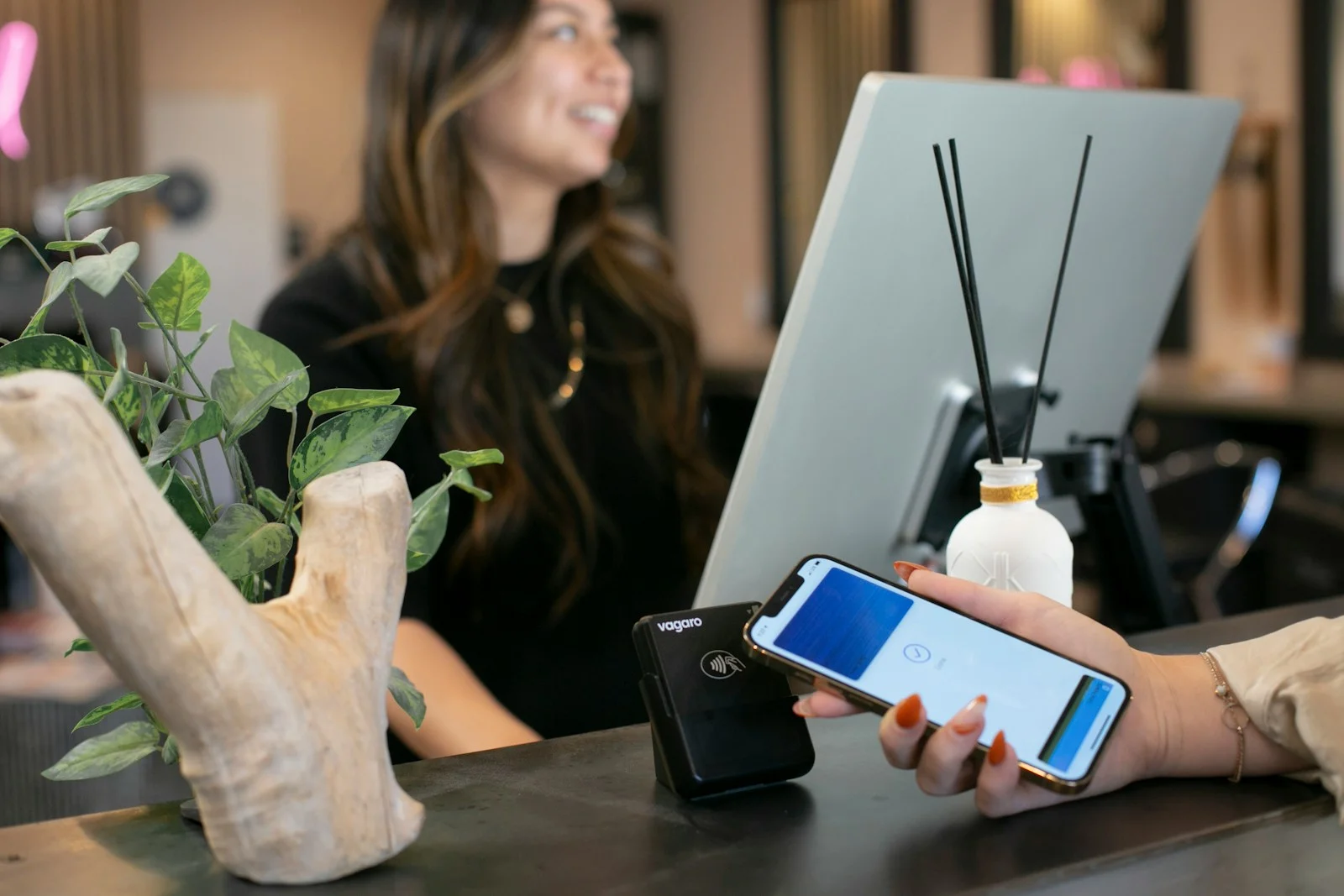

Mobile payment refers to the process of using a smartphone or wearable device to complete a financial transaction — either in a physical store or online. Rather than swiping a card or paying cash, customers use their mobile device, connected to a digital wallet, to authorise payments.

In practice, consumers pay using their phone through secure mobile wallet services linked to their preferred payment method.

The most widely adopted mobile payment solutions in Europe include:

- Apple Pay

- Google Pay

- Samsung Pay

- Bank-issued wallets (e.g. through native mobile banking apps)

- Contactless QR-based or tokenised systems

For in-store payments, devices use NFC (near-field communication) technology to transmit encrypted card data to a terminal. For online transactions, users can pay via phone directly within an app or browser, often confirming payment with biometric verification.

How to pay with your phone in 3 simple steps

- Add your payment method to a mobile wallet.

- Select the mobile payment option at checkout.

- Confirm the transaction using biometric authentication or device PIN.

This process allows customers to use phones to pay securely both online and in physical environments without entering payment details manually.

Why is mobile payment gaining popularity across Europe?

The shift towards mobile payments is driven by a mix of convenience, security, and changing consumer behaviour. According to recent studies by the European Central Bank and national regulators, the share of mobile wallet payments is increasing rapidly, particularly among younger generations and in urban areas.

Key advantages include:

- Speed – no need to pull out a wallet or insert a card

- Convenience – pay anytime, anywhere, with a device you already carry

- Security – biometric authentication adds a layer of protection

- Contactless experience – especially valued since the pandemic

Mobile payment aligns with Europe’s broader digital transformation in commerce — one focused on frictionless, user-friendly and secure transactions.

Consumers increasingly prefer to pay through mobile instead of traditional payment methods.

Are mobile payments secure? The facts behind the technology

Despite common concerns, mobile payments are among the safest ways to pay.

- Your actual card details are not stored on the device — instead, tokenisation replaces them with a one-time use encrypted code.

- All transactions require user authentication, via fingerprint, facial recognition, or device PIN.

- Many devices can be remotely wiped or locked in the event of loss or theft.

- Most modern payment gateways, like Fenige, include real-time transaction monitoring, risk scoring, and fraud prevention algorithms that enhance security on both the merchant and consumer sides.

Across Europe, regulators and payment providers continue investing in secure infrastructure supporting phone payments through tokenisation and strong customer authentication standards. In short, modern phone payments combine convenience with enterprise-grade security.

What does mobile payment mean for merchants?

For merchants — whether in retail, hospitality, travel or e-commerce — accepting mobile payments is now a critical expectation, not a luxury.

As more customers prefer paying with your phone, merchants must ensure their payment infrastructure supports modern mobile payment methods across channels and regions.

Offering popular mobile wallets such as Apple Pay or Google Pay can:

- Reduce checkout times and abandonment rates

- Increase conversion in mobile apps and websites

- Enhance customer satisfaction by offering familiar, trusted methods

- Support cross-border payments in multi-currency environments

With payment providers like Fenige, businesses can easily integrate mobile payment options into both online and physical points of sale.

These solutions allow customers to pay with mobile phones seamlessly while merchants maintain full transaction visibility and control.

Where can you pay using your phone?

Today, consumers can use phone to pay across a wide range of everyday scenarios, including:

- retail stores with contactless terminals

- public transport and ticketing

- online stores and mobile apps

- subscription and recurring services

- hospitality and travel payments

As mobile wallet services continue expanding across Europe, phone payments are becoming accepted across both physical and digital commerce environments.

Mobile payments in e-commerce – beyond brick-and-mortar

The rise of mobile commerce (m-commerce) means that most online shoppers now complete their purchases via mobile devices. For this reason, retailers must ensure their checkout processes are fully optimised for mobile payments.

Key recommendations:

- Enable “pay with one tap” options via Apple Pay, Google Pay, or other wallets

- Ensure the website or app is responsive and mobile-friendly

- Offer a choice of payment methods — including digital wallets, cards, and bank transfers

- Use a payment gateway that supports tokenisation and biometric authentication

When implemented correctly, customers can seamlessly pay through mobile without interrupting the purchasing journey.

Conclusion

Across Europe, mobile payments are rapidly becoming the default method for both online and in-person transactions. Consumers expect convenience, speed, and security — and mobile payment ticks all three boxes.

For businesses, embracing mobile wallets is an opportunity to improve conversion rates, customer loyalty, and operational efficiency. With modern payment platforms like Fenige, implementing mobile payment acceptance is straightforward, scalable, and future-proof.